Unit 4 - Notes

Unit 4: Regression

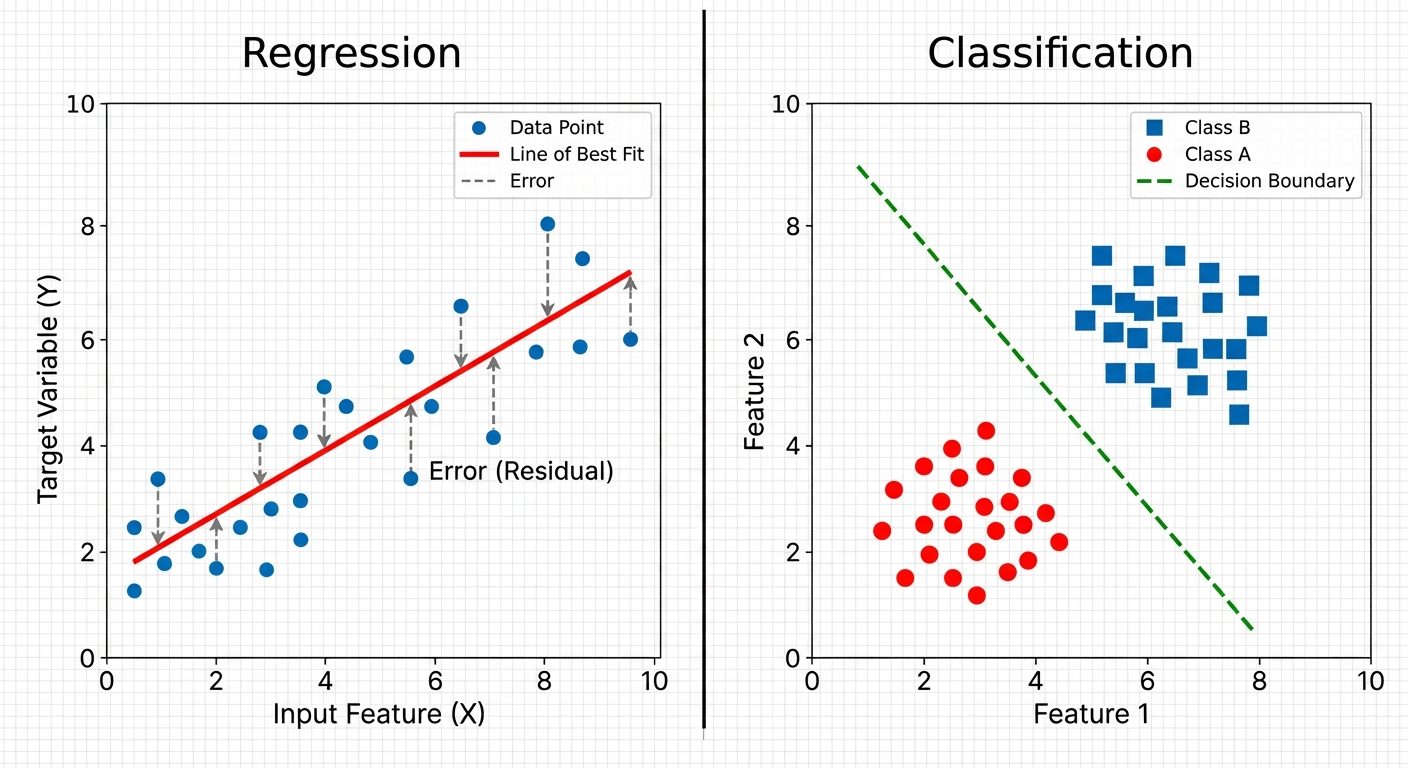

1. Regression vs. Classification

In supervised machine learning, the distinction between regression and classification lies in the nature of the target variable (output).

| Feature | Regression | Classification |

|---|---|---|

| Output Type | Continuous (numerical) values. | Categorical (discrete) class labels. |

| Goal | To predict a specific quantity (e.g., price, temperature, sales). | To predict group membership (e.g., spam/not spam, digit 0-9). |

| Evaluation Metrics | RMSE (Root Mean Squared Error), MAE (Mean Absolute Error), . | Accuracy, Precision, Recall, F1-Score, ROC-AUC. |

| Boundary | Fits a line, curve, or hyperplane through the data points. | Finds a decision boundary that separates data points into classes. |

Visualizing the Difference

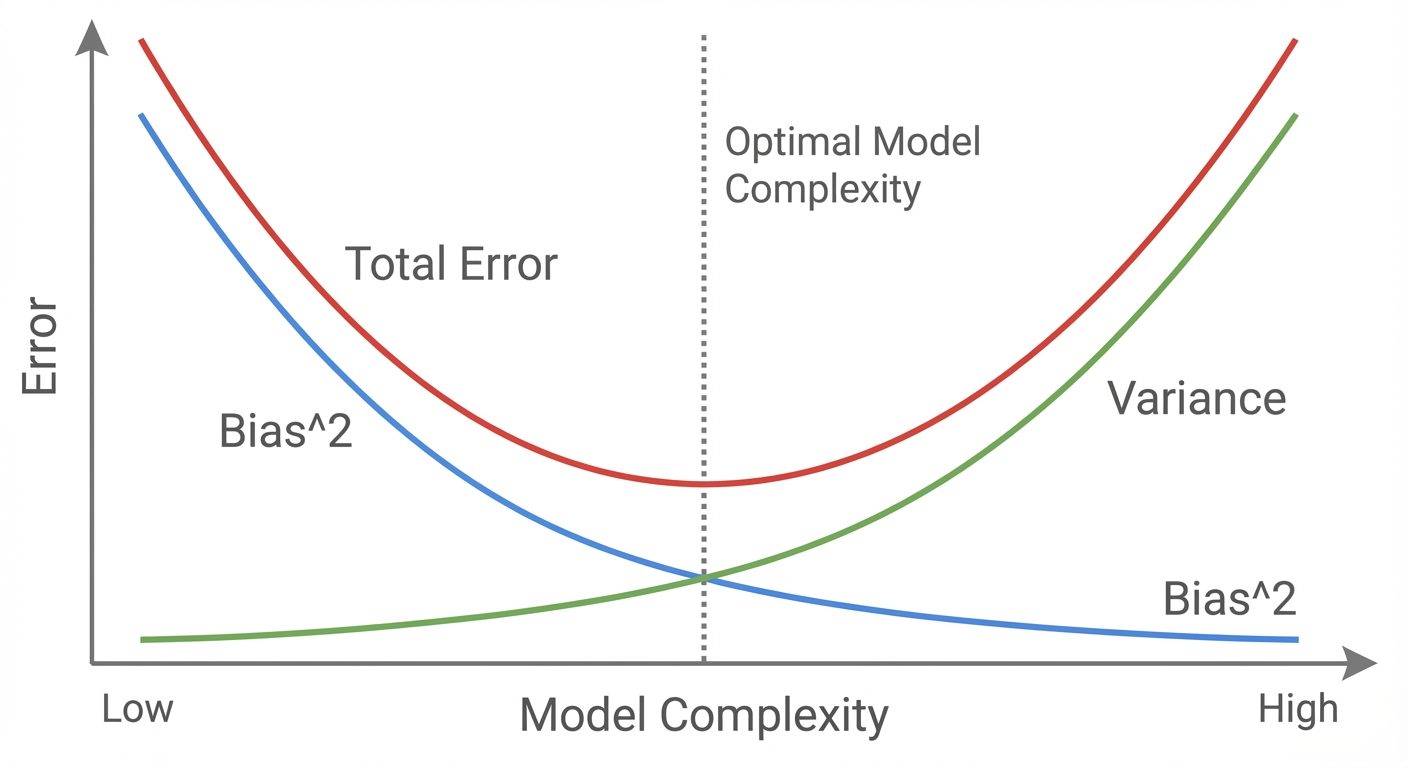

2. Bias-Variance Considerations in Regression

The bias-variance tradeoff is fundamental to understanding model generalization errors.

- Bias (Underfitting): Error introduced by approximating a real-world problem (which may be complex) by a much simpler model.

- High Bias: The model pays very little attention to the training data and oversimplifies the model. Example: Fitting a straight line to quadratic data.

- Variance (Overfitting): Error introduced by the model's sensitivity to small fluctuations in the training set.

- High Variance: The model pays too much attention to training data, capturing random noise rather than the underlying pattern. Example: High-degree polynomial passing through every data point.

Total Error Equation:

(Where is the irreducible error)

3. Simple Linear Regression (SLR)

SLR models the relationship between a single independent variable () and a dependent variable () using a straight line.

The Equation:

- : Intercept (value of when ).

- : Slope (rate of change).

- : Error term (residuals).

Cost Function (Ordinary Least Squares - OLS):

The goal is to minimize the Residual Sum of Squares (RSS):

Assumptions:

- Linearity: The relationship between and is linear.

- Independence: Observations are independent of each other.

- Homoscedasticity: The variance of residual is the same for any value of X.

- Normality: The error terms are normally distributed.

4. Multiple Linear Regression (MLR)

MLR extends SLR to include multiple independent variables ().

The Equation:

Matrix Form:

- The model fits a hyperplane in a -dimensional space rather than a line.

- Multicollinearity: A specific challenge in MLR where predictor variables are highly correlated with each other, making coefficient estimates unstable.

5. Interpretation of Coefficients

Interpreting values is crucial for inference.

- Intercept (): The expected value of when all predictors are zero. This may not always have a physical meaning depending on the data range.

- Slope Coefficients ():

- In SLR: A one-unit increase in is associated with a increase in .

- In MLR: A one-unit increase in is associated with a increase in , holding all other predictors constant.

Statistical Significance:

- p-value: Tests the null hypothesis that (no relationship). If , the predictor is statistically significant.

6. Polynomial Feature Expansion

When data shows a non-linear pattern (curved), linear regression can still be used by transforming the features. This is a form of Basis Expansion.

Concept:

Instead of fitting , we fit:

Although the relationship between and is non-linear, the model is still linear in parameters (), so OLS can still be used.

Implementation Example:

If input , a degree-2 polynomial expansion creates features: .

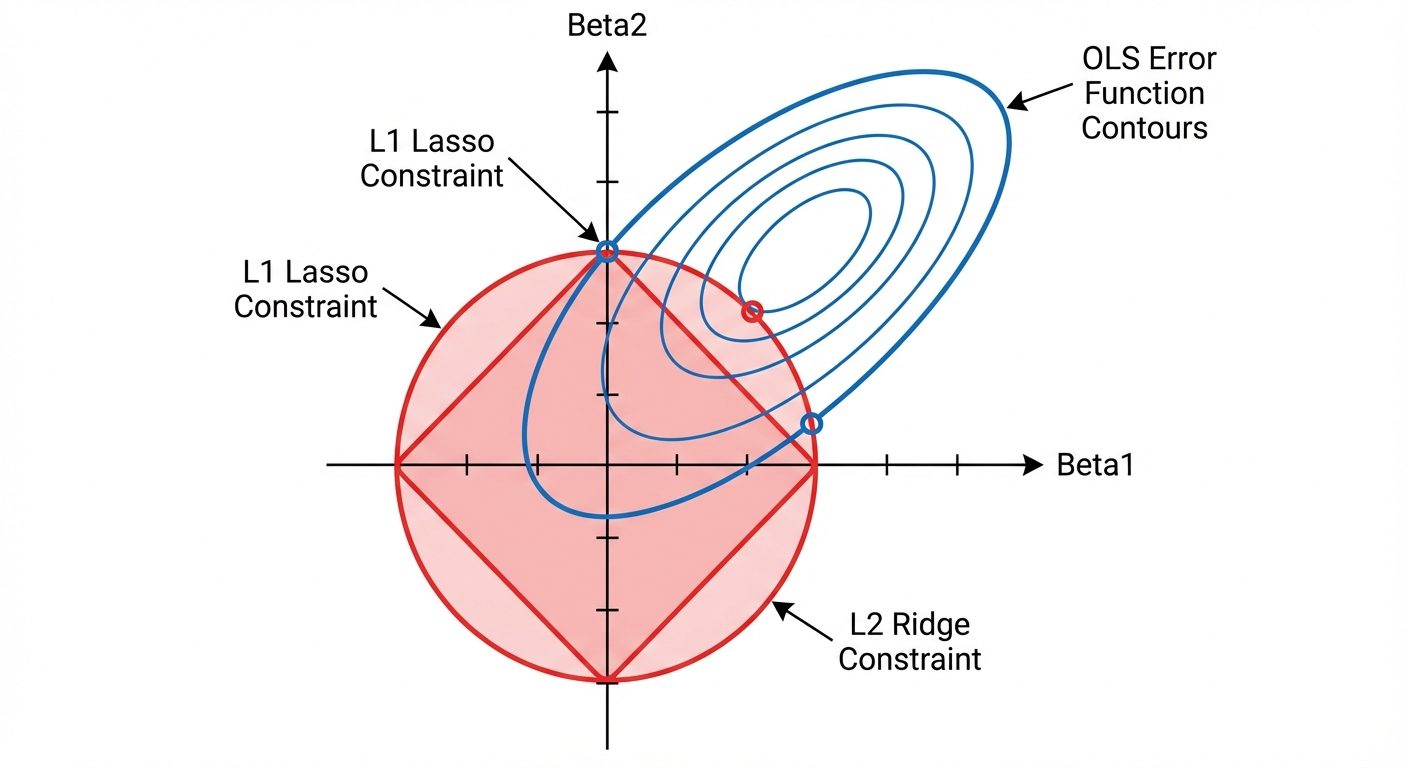

7. Regularized Regression Models

Regularization introduces a penalty term to the loss function to prevent overfitting by constraining the size of the coefficients.

A. Ridge Regression (L2 Regularization)

Adds a penalty equal to the square of the magnitude of coefficients.

- Effect: Shrinks coefficients toward zero but rarely exactly to zero.

- Use case: Good when many variables are correlated (handles multicollinearity).

B. Lasso Regression (L1 Regularization)

Adds a penalty equal to the absolute value of the magnitude of coefficients.

- Effect: Can shrink coefficients exactly to zero.

- Use case: Feature selection (produces sparse models).

C. Elastic Net

Combines L1 and L2 penalties.

8. Effect of Regularization on Model Complexity

The hyperparameter (lambda) controls the regularization strength.

- : Identical to OLS (No regularization).

- Small : Low Bias, High Variance. Model is flexible and can fit complex patterns.

- Large : High Bias, Low Variance. Coefficients are heavily penalized (shrunk). The model becomes very simple (flatter line).

- In Lasso, as , all coefficients become zero.

- In Ridge, as , all coefficients approach zero.

Selection: The optimal is usually selected via Cross-Validation.

9. Tree-Based Regression Models

Instead of a global linear equation, tree-based models partition the feature space into rectangular regions.

Decision Trees for Regression:

- Splitting: The algorithm recursively splits data based on feature values to minimize variance (usually MSE) within the resulting nodes.

- Leaf Value: The prediction for a new data point is the average (mean) value of the training samples falling into that leaf node.

Ensemble Methods:

- Random Forest: Builds many independent trees on bootstrapped data and averages their predictions (Bagging). Reduces variance.

- Gradient Boosting (e.g., XGBoost, LightGBM): Builds trees sequentially. Each new tree corrects the errors (residuals) made by the previous trees. Reduces bias and variance.

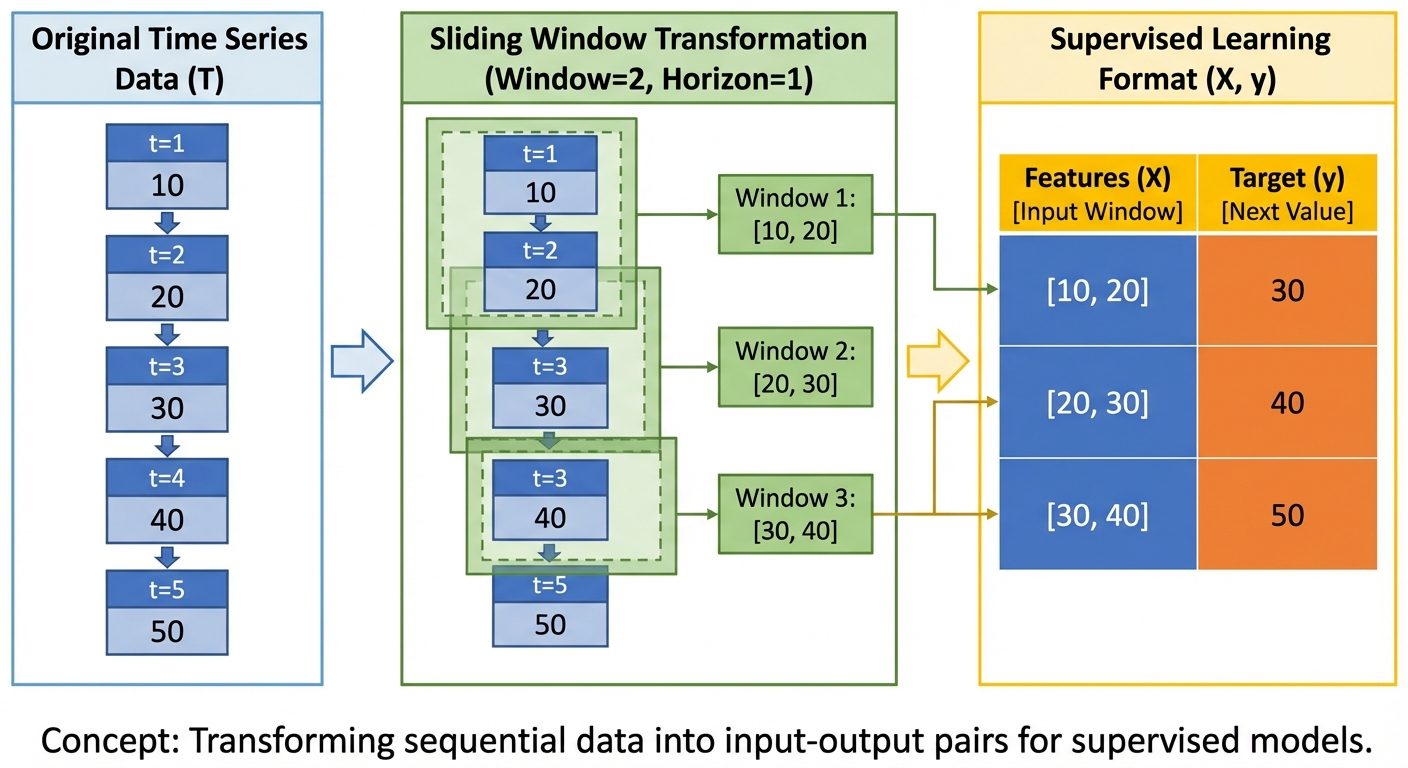

10. Time-Series Regression Models

Time-series regression involves predicting future values based on past history. The "independent variables" are often derived from the target variable itself.

Key Characteristics:

- Autocorrelation: Data points are not independent (today's price depends on yesterday's).

- Stationarity: Statistical properties (mean, variance) should ideally remain constant over time.

Feature Engineering for Time Series:

- Lag Features: Using as input to predict .

- Rolling Windows: Calculating moving averages or standard deviations over a window (e.g., past 7 days).

- Date-Time Features: Extracting components like Day of Week, Month, Quarter to capture seasonality.

Data Structure Transformation:

To use standard regression algorithms (like Linear Regression or Random Forest) on time series, the data must be transformed from a sequence to a supervised matrix.