Unit 6 - Notes

Unit 6: Blockchain Vertical Solutions and Use Cases

This unit explores how blockchain technology moves beyond theoretical concepts into practical, industry-specific applications (vertical solutions). It focuses on the disruption of traditional intermediaries in insurance, healthcare, asset management, finance, and currency.

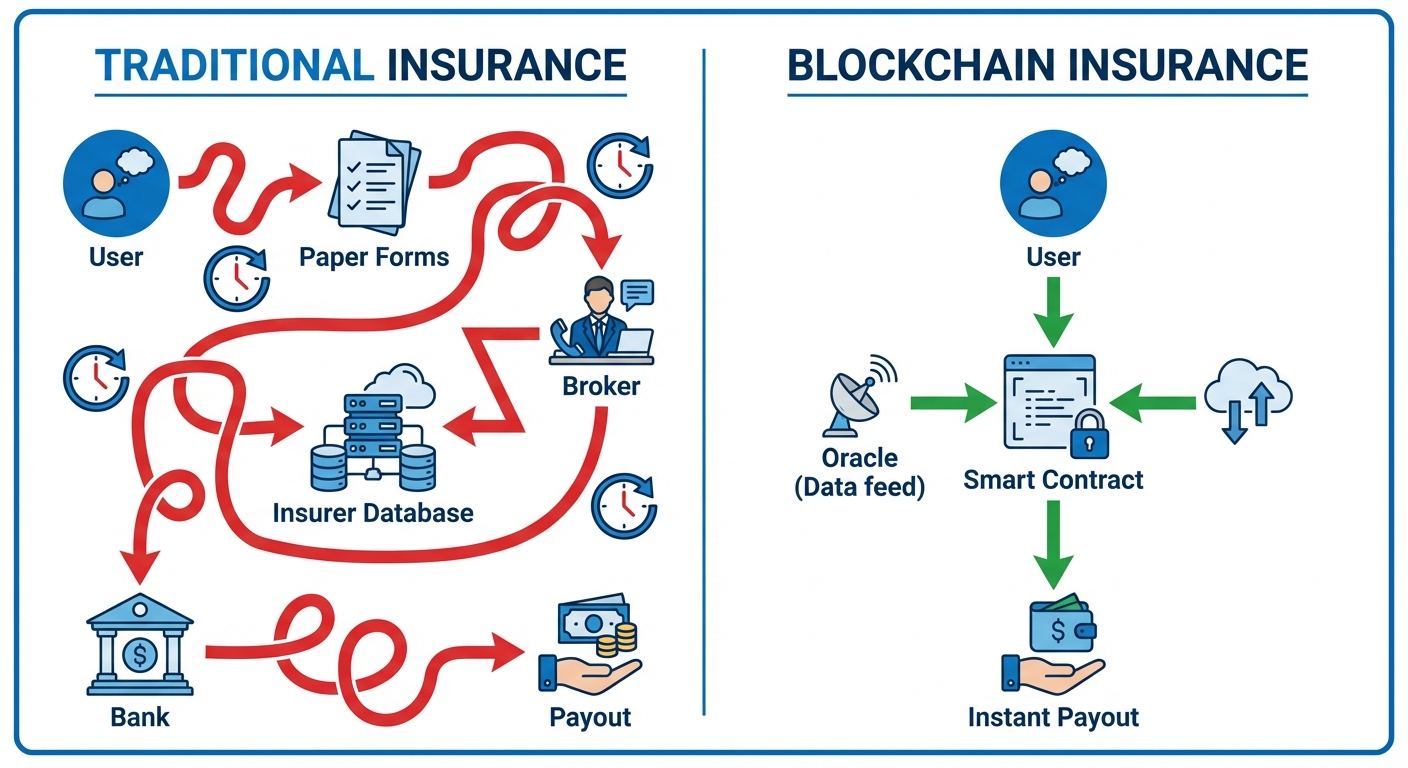

1. Blockchain in Insurance

The insurance industry is traditionally characterized by complex contracts, extensive paperwork, manual claims processing, and a high reliance on intermediaries (brokers). Blockchain introduces trust, transparency, and automation to this sector.

Key Challenges in Traditional Insurance

- Fraud: Costly and difficult to detect due to fragmented data.

- Inefficiency: Manual data entry and reconciliation slow down claim settlements.

- Human Error: Reliance on manual verification increases error rates.

- Lack of Transparency: Customers often struggle to understand policy logic or claim denial reasons.

The Blockchain Solution: Smart Contracts

Blockchain replaces traditional paper policies with Smart Contracts—self-executing code on the blockchain that automatically enforces the terms of an agreement.

Benefits

- Automated Claims Processing: Logic is pre-programmed. If condition is met, payout happens immediately.

- Fraud Detection: A shared, immutable ledger allows insurers to identify duplicate claims or suspicious patterns across the ecosystem.

- Parametric Insurance: Policies based on objective data triggers (e.g., flight delay insurance). If an Oracle (data feed) confirms a flight is delayed by 2 hours, the smart contract pays the policyholder instantly without a manual claim filing.

2. Life Insurance and Claim Processing (Case of Death)

Life insurance is a specific vertical where blockchain can alleviate the emotional and administrative burden on beneficiaries during the grieving process.

The Problem

In the traditional model, beneficiaries must locate the policy, obtain a physical death certificate, submit paperwork, and wait for manual verification. This process can take months.

Blockchain Workflow for Life Insurance

The architecture relies heavily on Oracles (trusted data feeds) that bridge the physical world (death registries) and the digital world (blockchain).

Step-by-Step Process:

- Policy Creation: The user purchases a policy. A smart contract is created holding the payout funds in escrow or linked to the insurer's liquidity pool.

- The Trigger (Death Registry): The blockchain connects to trusted government death registries or hospital databases via an Oracle.

- Verification: When the Oracle detects a death certificate issued for the insured identity, it pushes this data to the Smart Contract.

- Execution: The Smart Contract verifies the death certificate hash against the policy holder’s identity.

- Payout: The contract automatically triggers the release of funds to the beneficiary's crypto-wallet or bank account.

Key Advantages

- Certainty: Removes the risk of the insurer unfairly denying a valid claim.

- Speed: Reduces settlement time from months to days or minutes.

- Privacy: Zero-knowledge proofs can be used to verify eligibility without revealing unnecessary personal details.

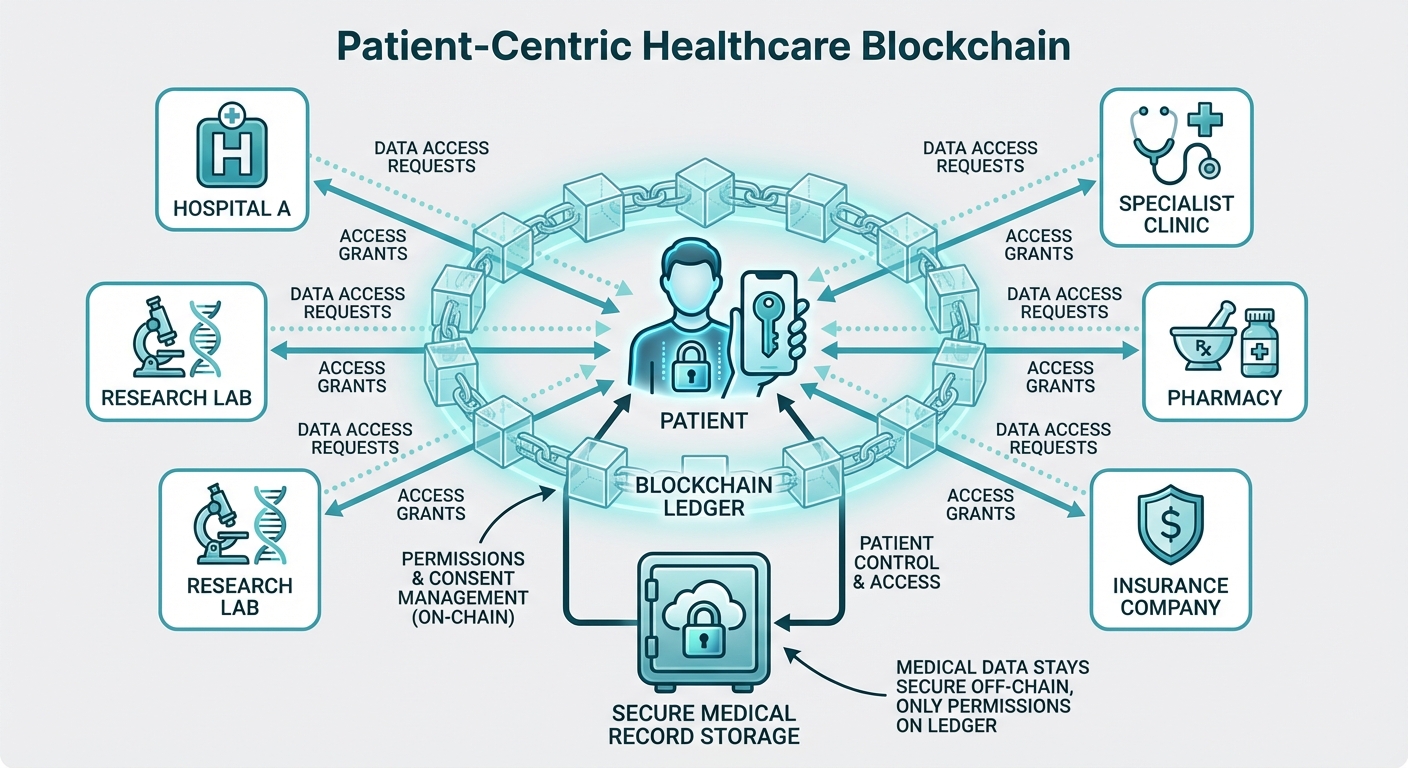

3. Blockchain in Healthcare

Healthcare systems suffer from data silos. A patient's data is scattered across various hospitals, clinics, and pharmacies, making it difficult to get a holistic view of patient health.

Electronic Health Records (EHR) on Blockchain

Blockchain does not store the actual medical data (which is too large and sensitive). Instead, it stores pointers (links) to data and manages access control permissions.

Architecture

- Off-Chain Storage: Medical images (X-rays, MRIs) and detailed notes are stored in secure databases (e.g., IPFS or secure cloud servers).

- On-Chain Metadata: The blockchain records the hash of the data (to prove integrity) and the access permissions.

Patient-Centric Interoperability

The core concept is Self-Sovereign Identity. The patient holds the private keys to their health data.

- Scenario: A patient visits a new specialist.

- Request: The specialist requests access to the patient's history.

- Grant: The patient approves the request via a mobile app (signing a transaction).

- Access: The specialist's system uses the temporary key to decrypt and view the records referenced on the blockchain.

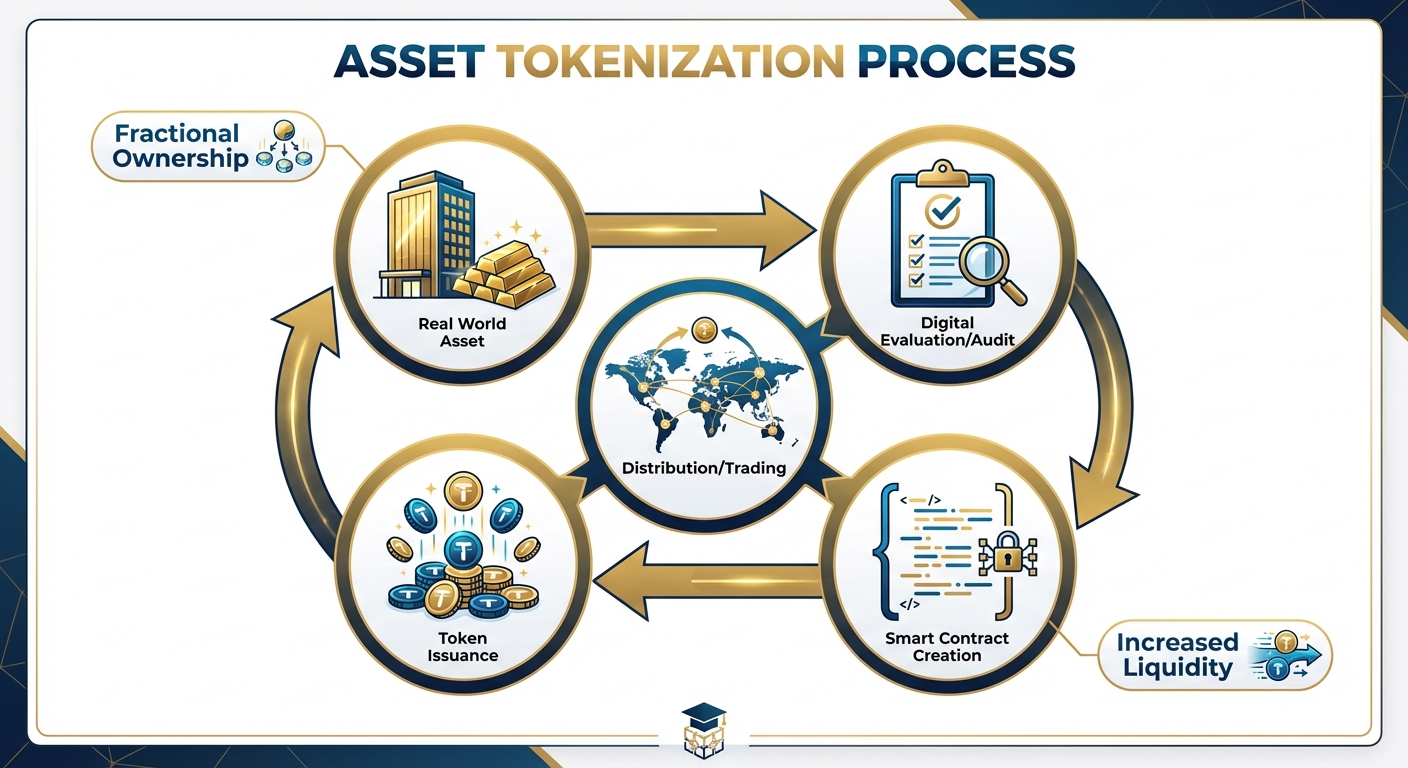

4. Assets Management

Asset management involves the administration of personal or corporate assets (stocks, bonds, real estate, art). Blockchain revolutionizes this via Tokenization.

Concept of Tokenization

Tokenization is the process of converting rights to an asset into a digital token on a blockchain.

Types of Managed Assets

- Tangible Assets: Real estate, gold, art, supply chain goods.

- Intangible Assets: Intellectual property, patents, copyrights, carbon credits.

Benefits in Asset Management

- Fractional Ownership: A high-value asset (e.g., a $10 million building) can be split into 10 million tokens of $1 each. This lowers the barrier to entry for investors.

- Liquidity: Traditionally illiquid assets (like real estate) can be traded instantly on secondary markets 24/7.

- Automated Compliance: Smart contracts can enforce regulations (e.g., KYC/AML checks) automatically before allowing a token transfer.

- Transparency: The provenance (history of ownership) is immutable, reducing the risk of purchasing stolen or counterfeit assets.

5. Financial Institutional Assets

This section refers to how banks and large financial institutions manage reserves, securities, and inter-bank settlements.

Clearing and Settlement

- Traditional Model (T+2 or T+3): When a trade happens, it takes 2-3 days to settle because different banks maintain different ledgers that must be reconciled by a central clearinghouse.

- Blockchain Model (T+0): Because all participants share a single distributed ledger, trade and settlement happen simultaneously.

- Result: Frees up capital that was previously tied up as collateral during the settlement period.

Trade Finance (Letter of Credit)

Trade finance involves complex paperwork to guarantee payment between importers and exporters.

- Blockchain Application: A shared ledger allows the importer, exporter, shipping company, banks, and customs to view the same real-time data.

- Automation: Once the shipping company updates the ledger that goods have arrived, the smart contract releases payment from the importer's bank to the exporter's bank.

Know Your Customer (KYC) and AML

Currently, every bank performs its own KYC checks. Blockchain allows for a Shared KYC Ledger. Once a user is verified by one trusted bank, that verification is stored (hashed) on the blockchain. Other banks can rely on this verification without repeating the expensive process.

6. Electronic Currency

Electronic currency in the context of blockchain refers to digital representations of value that function as a medium of exchange, unit of account, or store of value.

Categories of Electronic Currency

1. Cryptocurrencies (Decentralized)

- Examples: Bitcoin (BTC), Ethereum (ETH).

- Characteristics: No central authority; value determined by market supply/demand; permissionless access.

- Use Case: Speculative investment, censorship-resistant value transfer.

2. Stablecoins (Private/Pegged)

- Examples: USDC, USDT (Tether).

- Characteristics: Value is pegged to a fiat currency (usually 1:1 with USD) or a basket of assets.

- Mechanism: To maintain the peg, the issuer holds fiat reserves or uses algorithms to adjust supply.

- Use Case: shielding against crypto volatility while utilizing blockchain speed.

3. Central Bank Digital Currencies (CBDC)

- Examples: Digital Yuan (e-CNY), Digital Euro (concept).

- Characteristics: Issued and regulated by a nation's Central Bank. They are digital legal tender.

- Difference from Crypto: They are usually centralized (permissioned blockchain) and not anonymous.

- Goal: To improve payment efficiency, reduce the cost of printing cash, and enhance monetary policy implementation.

Comparison Matrix

| Feature | Cryptocurrency | Stablecoin | CBDC |

|---|---|---|---|

| Issuer | Community/Miners | Private Company | Central Bank |

| Volatility | High | Very Low (Pegged) | None (Fiat equivalent) |

| Decentralization | High | Low/Medium | None (Centralized) |

| Anonymity | Pseudo-anonymous | Varies | Low (Traceable) |

Summary of Unit 6

Vertical blockchain solutions are moving the technology from "experimental" to "essential infrastructure." Whether automating insurance claims via death registries, enabling patient-controlled health records, tokenizing real estate, or modernizing national currencies, the common thread is the removal of friction, reduction of intermediaries, and the establishment of a "Single Source of Truth."